“Can a divorce mediator give legal advice” is a trick question because “legal advice” has two entirely different meanings.

This often leads to confusion because people use the exact same words “legal advice” to refer to entirely different things.

The Meaning of “Legal Advice” for Lawyers and the Legal System: Legal Strategy

For divorce lawyers who litigate, “legal advice” is a technical term with a very narrow, special meaning. It refers only to the advice given by a licensed lawyer to a client with whom they have established an attorney-client relationship. It involves an attorney using expert legal knowledge or education to give strategic advice to a client that the client can use to his/her advantage, e.g., to avoid conviction on a criminal charge or to prevail in a contested divorce case.

This narrow, legal definition of “legal advice” is similar to the commonsense notion of legal strategy. When you hire an attorney to represent you, you pay them a lot of money and then they formulate and share with you a legal strategy, thereby giving you legal advice.

From this perspective, divorce mediators donot give legal advice. The ways mediators work, by definition, does not put them into a position where they even could give legal advice.

Mediators are working with a couple as a neutral third party. They do not enter into an attorney-client relationship with one spouse and offer them legal strategies to gain a strategic advantage over the other spouse. This is what lawyers representing clients do; it is not what mediators working for couples do.

The Meaning of “Legal Advice” for Non-Lawyers: Legal Information

In everyday usage, non-lawyers (who make up 99.99% of the population!) use the term “legal advice” to mean “legal information.”

Divorce mediators can and should give legal information to their clients! Such information might include:

how to calculate child support,

what county a divorce should be filed in,

whether the state is a “community property” state,

at what age children are considered emancipated,

whether alimony is presumptive in a state,

what issues need to be addressed in a separation agreement (e.g. parenting plan and division of assets),

how long it takes to get divorced, etc.

Without this information, a couple do not know what issues need to be understood, discussed, and addressed in order to make the decisions required for a legal divorce. From this perspective, divorce mediation lawyers–while remaining neutral–should give abundant “legal information.”

If your divorce attorney mediator declines to give you “legal information,” claiming that they cannot give you “legal advice,” you should find a new mediator.

Your goal is to choose a divorce attorney mediator who excels at the three things a mediator does:

The mediator manages interpersonal relations and conflict;

The attorney mediator communicates legal parameters and processes so clients can understand the issues they must address for their families and future; and

The mediator educates clients on financial issues so they can make informed decisions that will be a basis of the eventual court ordered divorce decree.

How to Find the Best Boston Divorce Mediator: Interpersonal Skills and Empathy

The best Boston divorce mediators exhibit empathy and compassion and can manage conflictual interaction, acknowledging painful emotions. At the same time, the mediator helps a couple move forward, step-by-step with the practical, concrete decisions that are the basis of a separation agreement. In other words, the mediator needs excellent interpersonal and communication skills.

The best way to judge the empathy and your fit with a mediator is to have a brief, no-cost (Zoom) interaction with them. You and your spouse must do this together, so neither of you feels like the mediator “belongs to” the other spouse. If you and your spouse do not feel comfortable with the mediator, or the mediator does not readily share the ways they work with couples or other legal information that you are looking for, the mediator is probably not a good fit.

Choosing the Best Divorce Mediator Near Me in Massachusetts: Legal Knowledge

A divorce mediation lawyer is a broker between the legal system, with its archaic traditions and language, and normal people who simply want a) what is best for their children, b) fair financial outcomes, and c) a predictable and secure path forward to their post-divorce lives.

The mediator uses their knowledge of the law to gently guide the conversation in a way that puts clients’ needs first. An expert attorney mediator writes the separation agreement in a way that meets legal standards and is clearly understandable to both you and the judge. Finally, this family law expertise allows the mediator to advocate with the court for you and your decisions if a court clerk, for example, mistakenly rejects your court documents or asks for clarifications.

When you call their office, do they answer your questions about divorce in ways that make sense to you and seem doable? Or do they communicate in a way that makes the legal parameters and process seem incomprehensible to a normal person?

Lawyers have traditionally presented the legal world as a mysterious one that you cannot understand. This empowers lawyers, but not you. Uncontested divorce can be clearly understood by the couples getting divorced, so your divorce mediator’s website should present all of this information to you clearly.

Choosing a Massachusetts Divorce Mediator: Financial Expertise and Client Education

A good mediator understands and can explain the financial dimensions of divorce, giving spouses a clear picture of their financial situation and the implications of different financial choices going forward. MA separation agreements have sections that focus on children and parenting, but otherwise focus overwhelmingly on financial issues and decisions. Divorce mediation is, in large part, financial mediation.

Your mediator should be able to display to you, in easily-understood numbers and charts:

your total assets and debts, and

the exact numbers and implications of any choices you make about support payments and division of property.

They should be able to display to you, in black and white numbers in real-time, the financial consequences of each scenario you discuss, e.g., “What if I kept the house, he kept his pension, and I kept the charge card debt?”

The mediator’s ability to present a financial overview and make clear the implications of each financial choice made by the couple is critical to creating a level playing field for making decisions about money. You cannot afford to use a relatively facilitative, passive divorce mediator who does not have financial expertise and experience or the skills to educate you about divorce finances.

It is not uncommon for a relatively dominant spouse in mediation to insist, “You’re taking everything and leaving me nothing.” It is much more difficult for that dominant spouse to persist in that claim if the couple and mediator are gazing at a spreadsheet that shows the division of assets to be exactly equal or even favorable to the dominant spouse who is claiming they are getting nothing.

Such clearly displayed financial facts can also encourage a less assertive or less financially savvy spouse to advocate for themselves. Even if such a spouse is not good with numbers or finance, he or she can see that getting 45% of total marital assets while their spouse is getting 55% is not equitable.

Evaluating a Divorce Mediator’s Financial Expertise

Does the attorney mediator give useful financial information on their website? Do they explain division of marital property in ways that you can understand?

When you call their office, do you get answers to your basic financial questions? If you ask how to divide a house that one of you owned before marriage, do they lay out in clear terms the ways divorcing couples can divide the value of such a house in a fair and equitable way?

If the mediator cannot communicate about the financial aspects of divorce in ways that make sense to you, you should choose a different mediator.

Pros and Cons of Divorce Mediation in Massachusetts

Many blogposts will list the benefits of divorce mediation, but this page also lists the most important cons. More importantly, it tells you how to avoid the cons by choosing an expert divorce mediator who can help you avoid them

The pros of divorce mediation are numerous:

It is much less expensive than hiring lawyers and litigating, and it is much less expensive than hiring two litigating lawyers to attempt to negotiate an uncontested divorce outside of court.

It is much faster than using the courts for a contested divorce.

It empowers you to be creative and make decisions tailored to you and your family. A good family law mediator gives you the tools to customize your separation agreement according to your family’s unique priorities and needs.

In contested cases, a judge does not have time to understand your situation or customize the divorce agreement in ways that work for both of you. They must keep cases moving. The judge will simply impose court orders about how you take care of your children, what happens to your property, and how much, if any, support will be paid.

It is less adversarial than the courts, which are set up as a competitive contest. Even the way cases are named, e.g. “Plaintiff/Defendant” or “Jones vs. Jones”, suggest a competition with winners and losers.

If you have children, mediation gives you practice in discussing and coming to agreement on the many practical issues that you will continue to face as your children grow and you co-parent after divorce.

It is more private than a contested case, where your finances and personal business are publicly discussed in court.

In a contested case, you will not know what is going on in court. You and your spouse understand your children’s needs, the value of your house, what belongings each of you wants to keep, and the importance of keeping health insurance. Unfortunately, once a case is on a contested track, none of this practical knowledge matters. Court motions, proceedings, and legal rules of evidence takes over, and you will have great difficulty understanding it.

Cons of Divorce Mediation in Massachusetts

There is one small disadvantage and two potentially major disadvantages to divorce mediation:

The small disadvantage is that hiring a divorce attorney mediator costs more money than doing the process yourself. Unfortunately, Massachusetts family courts have made the divorce process difficult to do yourself. The required court documents are poorly designed and confusing, making it very difficult to know what they are asking for, why they are asking for it, and what information goes where. Courts regularly reject DIY divorce filings over minor technicalities and don’t tell people how to fix them. Because court clerks are so afraid of giving “legal advice” (even though they are only giving “legal information”) they write messages such as, “We cannot give you legal advice. You should seek legal counsel” when they reject your filing.

The first potential major disadvantage of divorce mediation is that a dishonest spouse can more easily hide assets or financial information from the other spouse than they can in a contested case. Contested cases often begin with “discovery”, in which each spouse’s attorney requests 3-5 years of paystubs, credit card statements, bank statements, tax documents, business records, investment statements, property appraisals, insurance payouts, and records of debts, liens, and mortgages. This is a very long, inefficient, and expensive process. It does not guarantee that hidden assets will be found or that a complete financial picture will emerge, but it can make it more likely.

A family law mediator does not impose “discovery” on a couple, but the mediator can support a spouse’s request for particular disclosures. If a spouse in mediation requests to see financial statements or records from the other spouse, the mediator will support this request. The mediation lawyer, however, will not initiate the discovery process.

The honest spouse has some legal protection because the Financial Statements that are submitted to court are signed under penalty of perjury. If the financial statements are eventually found to be fraudulent, even after the divorce is final, financial aspects of the divorce agreement can be re-opened and litigated.

The second potential disadvantage of divorce mediation is that if you do not have one of the best divorce mediators in Massachusetts, a dominant or more forceful spouse can push a less assertive spouse into an agreement that favors the more forceful spouse. The separation agreement could favor the dominant spouse financially, in terms of parenting plan, or in other details. This is possible because mediators cannot advocate for one party or the other. If one spouse tends to be aggressive and insists on always getting their way in the marriage—and the other spouse regularly submits to this—this pattern can carry over into mediation. The resulting separation agreement can easily favor the more assertive partner.

For such marriages, it is very important to have an active attorney mediator who makes sure the couple understand legal parameters, rights, and standards. It is also important to hire a mediator who regularly and clearly illustrates, in black-and-white numbers, the fairness (or lack thereof) of financial decisions the couple are considering. (See how to choose a divorce mediator in Massachusetts.) Even a relatively unassertive spouse may be empowered to speak up for themselves if they can see that their spouse is trying to pay below standard amounts for child support or if the division of assets is not close to 50-50.

There are two final layers of protection for a less assertive spouse.

Each spouse is always welcome to consult with an attorney, who advises them on how to maximize their side of the equation in divorce. A person who feels like their spouse dominated them in their marriage can consult with an attorney after the mediator prepares the financial statements and an initial draft of the separation agreement. The consulting attorney can review the initial draft and frankly advise the less assertive spouse if the agreement seems fair and equitable. Such a consulting attorney can suggest ways a less assertive spouse could benefit from aggressive representation by an attorney in a contested case.

Armed with this information, the less assertive spouse can better advocate for themselves in the next mediation session. This information also allows a spouse to make informed decisions as they move forward with mediation. For many spouses, moving forward with a divorce quickly, affordably, and relatively amicably is more valuable than maximizing their position on every issue in the separation agreement.

The second and final layer of protection against a one-sided agreement is the judge who reviews and signs the separation agreement. It is only when the judge signs the agreement that it becomes a court order and the divorce decree is issued. The judge can and should reject the agreement if the judge determines it is unfair.

Finally, if either spouse stands before the judge and says, “I don’t think this agreement is fair and I don’t agree to it,” then the judge does not sign it and the case is dismissed. There is no divorce.

Combined alimony and child support orders and after-tax income in Massachusetts divorce

The purpose of this blog post is to illustrate a series of alimony, child support, and after-tax income scenarios following the steps required by the MA State Judicial Court 2022 Cavanagh v. Cavanagh decision. I show the calculations results for families with incomes ranging from $50,000 to $250,000 per year.

The Cavanagh decision upended established family court practice in which child support was calculated on the first $400,000 in family income (or the first $250,000 prior to 2021). Before Cavanagh, income that was used to calculate child support could not then be used to calculate alimony. This meant that divorcing couples with children (and less than $400,000 in family income) would have a child support order but no alimony order.

The Cavanagh decision ended the practice of limiting support orders for most families to child support only, and instead makes orders that include both alimony and child support a standard practice.

Cavanagh gave judges a specific set of calculations to consider in making alimony and child support orders. According to the Cavanagh decision, judges must do the following in making orders in contested (1B) cases where there might be child support:

Calculate alimony first…..Then calculate child support using the parties’ post-alimony incomes.

Calculate child support first. Then calculate alimony…[on family income above $400,000]

Compare the base award and tax consequences of the order that would result from the calculations in step (1) with those of the order that would result from the calculations in step (2), above.

After making these calculations, “The judge should then determine which order would be the most equitable for the family before the court, considering the mandatory statutory factors set forth in G. L. c. 208, § 53 (a), and the public policy that children be supported as completely as possible by their parents’ resources, G. L. c. 208, § 28, and determine which order to issue accordingly.”

The Supreme Judicial Court decision means that judges should do two very different calculations and choose the one that is “most equitable for the family.” The decision fails to define what “equitable” might mean or to give any examples of orders that might be more or less equitable.

The Cavanagh decision requires judges to do more work and to defend their decisions if they do not issue orders that include alimony (such orders are always higher than child support alone): “Where the judge chooses to issue an order pursuant to the calculations in step (2) or otherwise that does not include any award of alimony, the judge must articulate why such an order is warranted in light of the statutory factors set forth in § 53 (a).”

This may encourage judges to routinely combine alimony with child support orders. If they do not include alimony in their orders, they must defend their decision in writing and subject themselves to more scrutiny from appeals courts. In other words, the path of least resistance for judges is to make orders that use the calculations from Step 1, which calculates alimony first and then calculates child support based on post-alimony income.

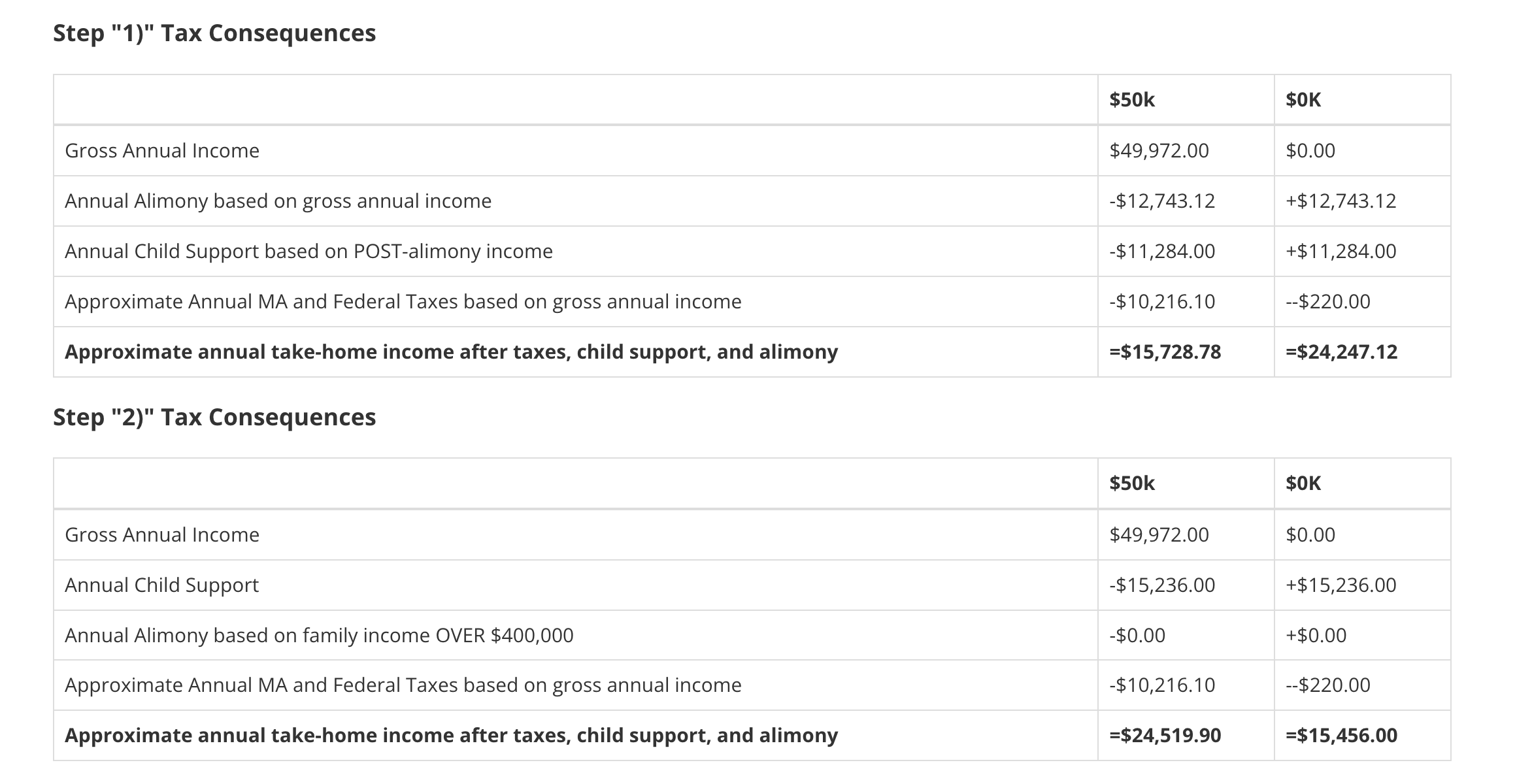

Scenario 1: Alimony and child support calculations with one spouse earning $50k per year and one spouse earning $0k per year

Click to enlarge

In this scenario, one spouse earns $50,000/year and the other spouse has no earnings. The spouse with no earnings (“$0k”) is the primary caregiver for the couple’s two children.

In the “Step 1”, or “alimony+child support” calculation, the higher earner pays $12,743 to the lower earner. The income of each is adjusted—the higher earner now has $12,743 less money per year and the lower earner has $12,743 more. These newly adjusted incomes are then used to calculate child support.

The higher earner (who has 1/3 or less of parenting time), pays the parent doing more childcare $11,284 per year. Finally, the approximate taxes are calculated—the higher income parent pays $10,216, while the lower earner gets $220 tax credit. Taxes are on gross income only. Alimony (since 2019) and child support play no role in taxes. The payor of alimony and child support does not receive any deduction for them, and the recipient of child support or alimony pays no taxes on the money received.

This alimony+child support calculation results in an approximate after-tax income of $15,728 for the higher earner and $24,247 for the lower earner, who has primary childcare responsibilities for two minor children.

In the “Step 2”, or “child-support-only”, calculation, only child support is paid, resulting in a payment of $15,236 to the parent who has the child 2/3 or more of the time. Taxes remain the same as in the alimony+child support calculation. The child-support-only calculation for this family reverses the income situation almost exactly: the higher earner has about $24,519 in after-tax income, while the lower earner, taking care of two children, has only $15,456.

In this scenario, alimony+child support would leave all family members living at or just above the federal poverty guideline levels. Child-support-only would leave the children and their caregiver well below federal poverty guidelines.

The difference for each party between alimony+child support and Child-support-only is about $9,000/year.

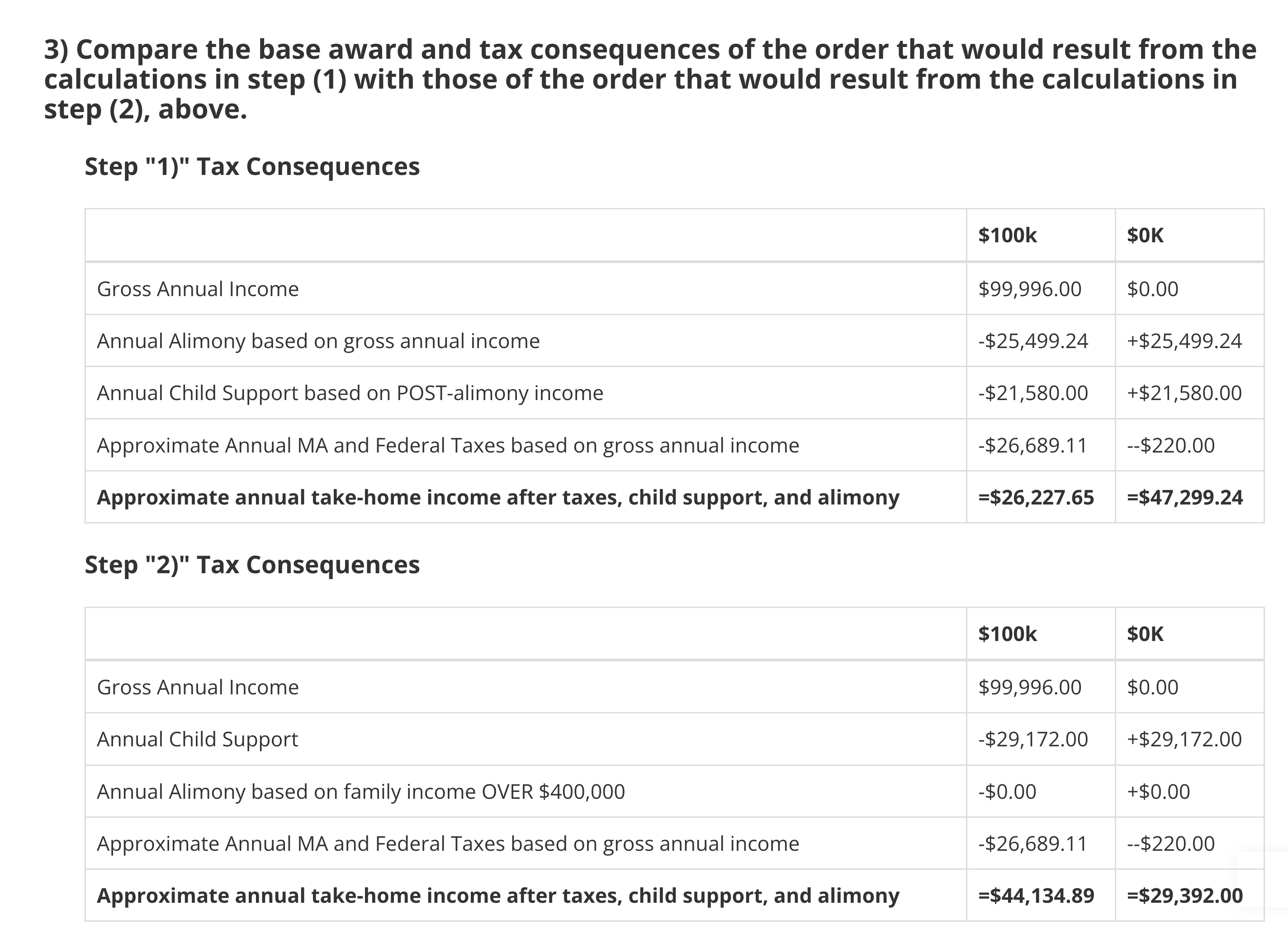

Scenario 2: Alimony and child support calculations with one spouse earning $100k per year and one spouse earning $0k per year

Click to enlarge

In this scenario, one spouse earns $100,000/year and the other spouse has no earnings. As in each of these scenarios, the spouse with lower earnings (“$0k” in this case) is the primary caregiver for the couple’s two children.

In this scenario, the difference between alimony+child support and child-support-only is more substantial. Child-support-only—which represents the way support was awarded up until the Cavanagh decision—gives the higher earner $44,134. This places the higher earner at the low end of middle-class status for Massachusetts. The parent taking care of the children, with $29,392 lives at just $5,000 above the federal poverty line.

Alimony+child support, in contrast, gives more income to the caregiver and children: $47,299. This puts them well above the poverty line ($24,860 for a family of three), but below middle-class status (about $70,000 for a household of 3). The higher earner ($29,392) lives $15,000 above the poverty line, but below middle-class status.

Scenario 3: Alimony and child support calculations with one spouse earning $100k per year and one spouse earning $50k per year

Click to enlarge

As in Scenario 1, the difference between alimony+child support and child-support-only is only $9,000 for spouses.

In Scenario 2, in contrast, the difference between Steps 1 and 2 was $18,000. This is because Scenario 2 had a bigger difference in incomes, which affects both alimony and taxes. Alimony is calculated as a percentage of the difference between incomes, so a difference of $100,000 gives alimony that is twice as large as when the difference in incomes is only $50,000. In addition, income tax is progressive, so the $100k earner pays MORE than twice as much in taxes as the $50k earner.

In this example, alimony+child support puts the caregiver and children into the middle class and the high earner just below middle class. Child-support-only would put the high earner and low earner at the low end, or just below, middle class status.

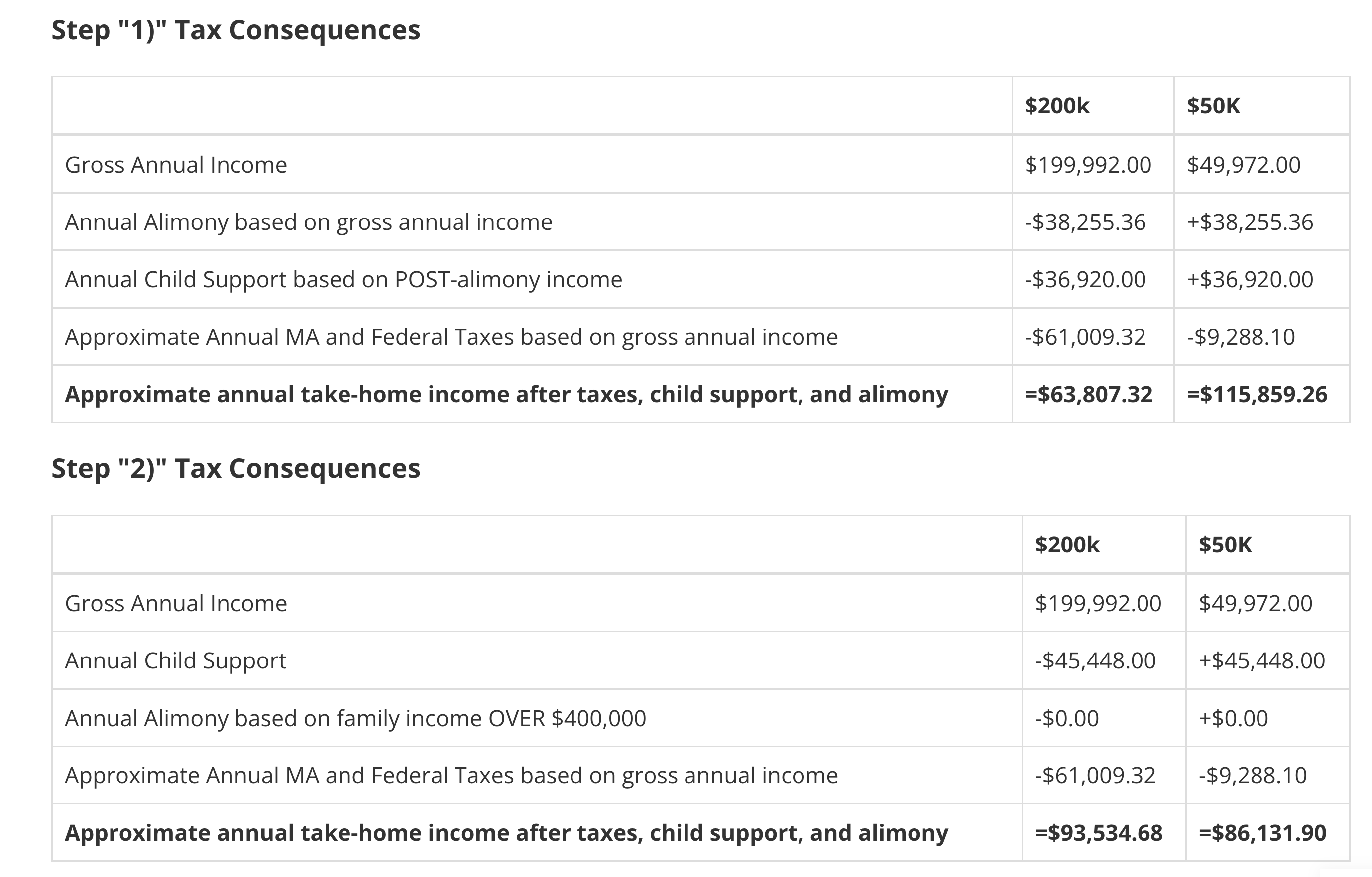

Scenario 4: Alimony and child support calculations with one spouse earning $200k per year and one spouse earning $50k per year

Click to enlarge

With this high family income ($250k) and large difference between spouses in earnings ($200k), the difference between alimony+child support and child-support-only grows to $30,000. The high earner pays relatively high alimony, child support, and taxes. This results in approximate take-home income of $63,807 for the high earner despite the relatively high $200,000/year salary.

Both calculations leave both parties with middle class income. The alimony+child support makes the caregiver and children upper middle class, while the child-support-only calculation makes the high earner upper middle class and leaves the caregiver and children more precariously middle class.

Divorce mediation checklist: How to Prepare for Divorce Mediation

1) The first checklist item for preparing for divorce mediation is:

Relax

By choosing divorce mediation instead of fighting in court with lawyers, you have already made a great choice. With mediation, your divorce can be relatively fast and inexpensive, and the process, unlike fighting in court, does not turn you into enemies. If you have children, using mediation will help you reach an agreement that helps you both to co-parent after divorce even as you move forward with your lives.

Another reason to relax is that you—not a court scheduler, a $400/hour divorce attorney, or a judge—control the process. You can schedule meetings when it fits your schedule and file papers with the court when you are ready.

The hallmark of divorce mediation is that you, yourselves, make the decisions that go into the divorce agreement. Nothing is forced on you and there are no legal “gotchas”.

In divorce mediation, the mediator facilitates your discussions and informs you about divorce laws and divorce financial issues, but nothing goes into the divorce agreement unless you both agree to it. This helps couples using divorce mediation to make reasonable decisions despite the emotional turmoil of disentangling from each other.

Are you worried that you are giving up rights by doing mediation? Relax again.

You give up no rights by doing divorce mediation. You are always able to leave mediation and pursue a contested divorce (fighting in court). You are also always welcome to consult with an outside attorney, whom you are paying to promote your specific, individual interests, even as you work with your spouse and a mediator.

A final reason to relax is that nothing is final with your divorce agreement for months. You can revise your agreement if you like, even after you have signed it and sent it to court.

It takes 1-3+ months to be scheduled for the 10-minute court hearing where a judge reviews your court documents and asks you if you have read the agreement, you understand it, and you agree to it. It is only when you and your spouse both say, “I agree”, that the judge signs the paperwork and your divorce has legal force.

2. Choose a Divorce Mediator Who is a Divorce Attorney

In Massachusetts, there is no legal standard or licensing for private divorce mediators. (You yourself could create a website and claim you are a divorce mediator!) Lawyers, in contrast, must attend law school, pass the bar exam, and maintain a license. Since getting divorced is fundamentally a legal process, you want a lawyer who understands the legal parameters and issues involved in divorce and can translate them into plain English for you so you can make informed decisions. A lawyer is also much more likely to be able to write a separation agreement that meets legal requirements for divorce.

3. Understand the divorce mediation process and steps in a nutshell

You meet with the mediator, and she informs you about the issues that have to be addressed and decided when you get divorced. She facilitates your conversations and helps you keep emotions in check as you work through each issue, one at a time.

After the first meeting, Attorney Rueschemeyerprepares all court documents, reflecting your decisions. There are five to seven required documents, depending on whether or not you have minor children. At the second meeting, you finalize decisions, and she goes over them with you, making sure you understand them.

You sign and mail the documents to court.

After one to three months waiting for the first available hearing, you have a 10-minute hearing where the judge asks you if you understand and agree to what is in the separation agreement. The judge then signs the documents.

The divorce agreement has immediate legal force when the judge signs it, but it only becomes “absolute” (meaning you can remarry and that you can file taxes as “single”) 120 days after your hearing date.

4) Understanding the three basic issues that get negotiated

The “big three” issues that need to be figured out for any divorce are:

If you have children under age 18, you will decide on a parenting plan that lays out who takes care of the child(ren) when. Your parenting plan can address not just a weekly schedule but also holidays or other special days. Since you are the ones devising the schedule, you can customize this schedule in ways that work for you.

4b) Division of assets and debts

Property acquired and debts incurred during the marriage generally “belong” to both of you, regardless of whose name is on a particular asset or debt. When you get divorced, the ownership of each asset and responsibility for each debt is specified in the divorce agreement, and you then no longer have “marital assets”, i.e., assets that belong to both of you by the fact of being married.

Massachusetts is not a “community property state” where there is a clear, legal distinction between “pre-marital” property and “marital” property, but in practice, it typically operates the same way as in community property states. The law in Massachusetts says that division of property must be “fair and equitable.” At least some judges treat “fair and equitable” to mean 50%-50% of marital property, exactly the same as it would be in a community property state.

4c) Support

Support comes in two basic forms:

child support (if you have children under 18, or dependent children under 23), and

alimony

Child support is “presumptive” (standard or assumed) in Massachusetts and calculated according to a state formula. The state can take an active role in collecting child support, e.g., by collecting it directly from paychecks before they reach the parent who is paying the child support.

Alimony is not presumptive. The state gives a messy list of factors that should be considered when determining whether alimony should be awarded, but it does not say how those factors should be evaluated or weighed. There is a maximum alimony formula which puts limitations on the amount and duration of general term alimony, but the guidelines do not calculate what alimony should be, or if alimony should be awarded at all.

Finally, since the August 2022 Cavanagh vs. Cavanagh decision, judges in contested cases (but not mediated ones) must consider awards that combine alimony and child support .

In addition to the “big three”–parenting plan, property division, and support–you will also discuss and come to agreement on:

the timing of post-divorce events (moving apart, selling a house, transferring car titles, changing cellphone plans, etc.),

health insurance,

taxes,

(if you have children) paying for college and for life insurance to benefit the children,

pets, and

other relevant issues.

5) Become familar with the basic financial parameters for child support and alimony

Before you begin mediation, I invite you to experiment with this alimony calculator and this unique combined-child-support-and-alimony calculator. These are the only calculators on the web that take into account taxes and allow you to approximate the take home income as payor or recipient of child support or alimony. These will give you a sense of the range of financial outcomes your decisions about support in mediation could have. This puts you in a much better position to discuss support amounts that work for both of you.

In divorce mediation, you are always welcome to consult with an outside attorney. Unlike a mediator, who must remain neutral, the consulting attorney can encourage you to advocate for yourself and try to maximize (even if it is not realistic) your side of the equation in the divorce agreement. If you think you might want to do such a consultation, you can screen attorneys and then set up an appointment for after you have received the initial draft of all the documents. This allows an outside attorney to see the full package–both financial statements and all the details–in order to advise you.

7) Find the original or obtain a certified copy of your marriage certificate

You cannot get divorced in Massachusetts without submitting a marriage certificate with other required court documents. The marriage certificate will not be returned to you. You can order a certified copy of your marriage certificate online from this mass.gov site.

8) Gather financial information that will go into the required court Financial Statements

Gathering all the financial information can take some effort!

The following is a list of documents or financial figures that you will use to provide information for Attorney Rueschemeyer to fill in your Financial Statements.

The Financial Statements, along with the Separation Agreement, are the most important court documents. They lay out your income, assets, and debts, giving a detailed picture of your financial situation. The judge uses these financial statements to evaluate whether the division of assets is “fair and equitable” and whether the alimony/child support figures in your Separation Agreement fall within legal parameters.

In an uncontested case, you do not need to submit any of the financial documents listed below to the court. The judge and court clerks consult the Financial Statements, which contain a summary of information from all these diverse documents. You will sign the Financial Statements under penalty of perjury, attesting that they are complete and the information in them is truthful.

Attorney Rueschemeyer collects all of your financial information in an online questionnaire that you fill out before meeting with her, and then uses custom software to translate your answers into the Financial Statements. You will need to consult documents or websites listed below in order to provide financial information in Attorney Rueschemeyer’s pre-meeting, online questionnaire.

You should be prepared to share any or all of these documents or website financial information printouts with your spouse if they request it.

Your most recent paystub (or a typical recent paystub if the most recent one isn’t typical), in order to provide income, taxes, deductions, and withholding.

W-2 for the most recent tax year, simply to provide W-2 income from that year.

Documents that show any other income, including social security, disability, or retirement

If either of you is self-employed or has rental income, be prepared to show your 1040 for the most recent tax year. If you don’t have your 1040 but you are self-employed, share your Schedule C and (if you have rental property income) Schedule E

Names and balances of retirement accounts

Information about traditional pension(s) (common among teachers and public employees). We can quickly calculate the present value of your pension if, before our meeting, you ask your pension administrator this question: “How much would my monthly benefit be at retirement if I a) stopped working now, but b) waited until normal retirement age to start collecting the benefit?”

Names and balances for all savings or checking accounts or CDs or brokerage accounts or stocks or bonds.

List of debts, including credit card debt. Include the amount owed and the name of the company you owe it to.

Amounts owing on car loans

Value of cars. You can look up the ‘private party value’ at www.NADA.com or simply agree on an approximate value

‘Fair market value’ and the ‘tax assessed value’ of houses or other real estate that is in either or both of your names. You can find the “tax assessed value” on your town government’s website, and you can use Zillow or an appraiser to determine “Fair Market Value.” (You will probably only use an appraiser if you cannot agree on a Fair Market Value.)

The amounts of any mortgages owing on properties you own

The approximate number of years that each of you has paid into Social Security (You can get an exact number by creating a “my social security account” at https://www.ssa.gov/myaccount, but it is takes some time and effort to set up passwords for the site).

Any prenuptial agreement (less common).

Names, amounts, and vesting schedules for any stock options or RSUs (less common)

If health insurance from your job covers your spouse, ask your Human Resources person this question: “Can my spouse stay on my health insurance after my divorce if there is a Court Order to keep them on it?” (This question is for information—even if your spouse could stay on it, it does not mean that the divorce agreement you agree to will keep them on it.)

If you have a traditional pension(s) (common among teachers and public employees): I can calculate the “present value” of your pension if, before we meet, you ask your pension administrator this question: “How much would my monthly benefit be at my normal retirement age if I a)stopped workingnow, but b)waiteduntil my normal retirement age to start collecting the benefit?”